Bookkeeping

Footings Definition, What is Footings, Advantages of Footings, and Latest News

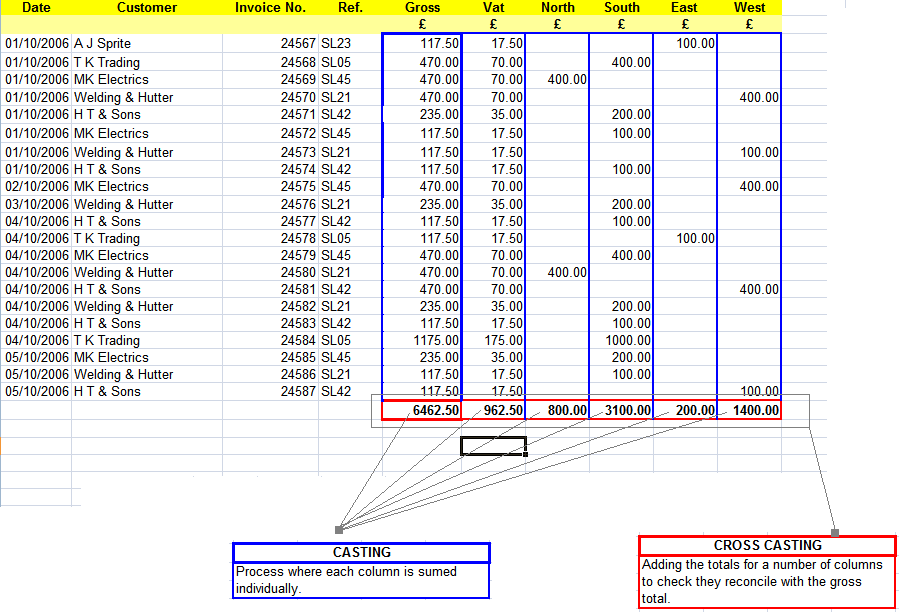

If you have a table of values, with both columns and rows, you can cross-foot to double-check your numbers. This means adding together all the column foots, footing in accounting and then comparing the result with the sum of all the rows in the table. You don’t need to foot a column if there is only one entry in the column.

A guide to basic accounting for manufacturing businesses

The net amount is reported on the company’s financial statements for the period. Spreadsheets lay out numbers in rows and columns, each of which can be totaled. Imagine a sheet showing monthly sales revenue for five products over the course of a year. Each of the five rows reports one product and each of the 12 columns reports one month.

Calculation and Use of Footings

This simple yet powerful method allows accountants and financial professionals to present and interpret information more efficiently. By calculating the total amount of a specific category or column, footing provides a clear and concise summary that facilitates decision-making processes. Overall, footing in accounting is a pivotal technique that enables the concise presentation of financial data. By calculating the total amounts within columns, accountants can provide a snapshot view of key figures, facilitating improved analysis, decision-making, and financial reporting. In the world of accounting, footing refers to the process of calculating the total values in a column or a group of related items. It involves the addition or summation of numerical data to derive a final total.

Crossfooting

Footnotes to the financial statements refer to additional information that helps explain how a company arrived at its financial statement figures. They also help to explain any irregularities or perceived inconsistencies in year to year account methodologies. It functions as a supplement, providing clarity to those who require it without having the information placed in the body of the statement.

In general, accountants must foot many different columns of data in order to find a total for a particular period of time or of a certain piece of information. It is also important when verifying that data or information is correct. Let’s say the T-account listed below shows the inventory transactions for Macy’s (M).

- For example, footnotes will explain how a company calculated its earnings per share (EPS), how it counted diluted shares, and how it counted shares outstanding.

- It involves the addition or summation of numerical data to derive a final total.

- The debits are first tallied, followed by the credits, and they are netted to calculate the account balance.

- Often, the footnotes will be used to explain how a particular value was assessed on a specific line item.

crossfoot

This information can then inform marketing strategies, inventory management, and resource allocation. These are just a few examples of the types of footings employed in accounting. The choice of footing depends on the specific purpose of the analysis, the structure of the financial data, and the desired level of detail and comparison. The term “footing” originated from the practice of writing the final sum at the foot or bottom of a column.

This visual representation made it easier for accountants to quickly reference and comprehend the totals. While the advent of modern accounting software has made footings less apparent in physical documents, the concept still holds immense significance in the digital age. Footing information simply means to add together all of the data in a particular column.

Often, these will refer to large-scale events, both positive and negative. For example, descriptions of upcoming new product releases may be included, as well as issues about a potential product recall. Often, the footnotes will be used to explain how a particular value was assessed on a specific line item.

Clear can also help you in getting your business registered for Goods & Services Tax Law. Christine Aldridge is a financial planner who has been writing articles related to personal finance since 2011. She has bachelor’s degrees in political science from North Carolina State University and in accounting from University of Phoenix.

By totaling each section, footings provide insights into the sources and uses of cash, facilitating analysis of cash flow patterns and management of liquidity. Footing, in the context of preparing a trial balance, refers to the process of verifying the accuracy of the total debit and total credit amounts recorded in the general ledger. It ensures that the fundamental accounting equation, where the sum of all debits equals the sum of all credits, is maintained. The two footings are netted together to arrive at the account balance for inventory.

Footing is predominantly used in financial statements, spreadsheets, and other accounting documents to provide a concise representation of cumulative figures. The debit column is on the left side of the account while the credit column is on the right. Amounts are entered to these columns as business transactions are recorded and posted.